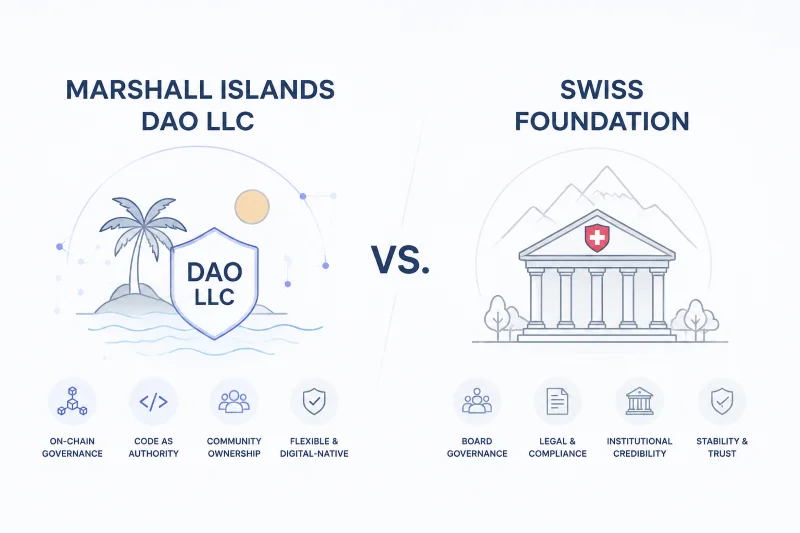

Marshall Islands DAO LLC vs. Swiss Foundation: Full Comparison

A comparison of the Marshall Islands DAO LLC and Swiss Foundation, explaining how each legal structure differs in governance, cost, compliance, and suitability for different types of Web3 and crypto projects.

The Crypto Valley Top 50 report, CV VC, Q1 2026 places the combined valuation of Switzerland's top blockchain entities at approximately $593 billion, with the Ethereum Foundation, Solana Foundation, Polkadot's Web3 Foundation, and Cardano Foundation all domiciled in Zug. The Swiss Foundation built Crypto Valley. Its institutional credibility is real, its banking relationships are unmatched, and its track record speaks for itself.

But that track record belongs to a different era of protocol development. The projects that chose Swiss foundations in 2014-2020 were building infrastructure before on-chain governance existed as a concept. Today's protocol teams are choosing between a structure designed for institutional stewardship and one designed for algorithmic, token-native governance from the ground up.

That choice is what this article is about. Both the Marshall Islands DAO LLC and the Swiss Foundation provide legal personhood, asset protection, and a framework for operating a blockchain project. They are built on different legal philosophies, for different types of organizations, at meaningfully different cost points. Here is the complete comparison.

What Is Each Structure, and Who Is It Actually For?

The Marshall Islands DAO LLC is a digital-native legal entity built for DAOs. The Swiss Foundation (Stiftung) is a traditional civil-law structure adapted for blockchain ecosystems. Choosing the right one depends on your governance model more than your jurisdiction preference.

The Marshall Islands DAO LLC

The Republic of the Marshall Islands enacted the DAO Act of 2022, becoming the first sovereign nation to build a legal entity from the ground up for how DAOs actually work. The RMI DAO LLC lets a project track membership through tokens rather than a member registry, allows smart contracts to serve as the governance mechanism, and explicitly supports manager-less operation where on-chain governance is the source of authority rather than a human manager.

The structure comes in two variants. The non-profit DAO LLC is tax-free at the entity level, and governance tokens issued under it, where those tokens carry no economic rights, are explicitly not treated as securities under RMI law. That is written into the 2023 Amendment, not a legal opinion. The for-profit DAO LLC is subject to a 3% Gross Revenue Tax on revenue generated outside the Marshall Islands, excluding capital gains and dividends.

MIDAO operates as the exclusive public-private partnership with the RMI government for DAO LLC registration, with 250+ entities registered and clients including Pyth Network, MetaDAO, Gnosis Guild, and ApeCoin Governance.

The Swiss Foundation (Stiftung)

The Swiss Foundation is the most prestigious offshore option for blockchain projects. Ethereum, Solana, Polkadot, Cardano, Cosmos, and many foundational L1 protocols chose Swiss foundations, drawn by political stability, a sophisticated legal system, and a mature banking ecosystem that understands crypto.

Under Swiss civil law, a foundation is formed by notarial deed with an initial endowment of approximately CHF 50,000 and is governed by a Stiftungsrat (board of trustees) of at least three members. At least one board member must be domiciled in Switzerland, making the structure inherently onshore with real local substance requirements.

The foundation is purpose-locked: the Zweck (stated purpose) is legally binding at formation, and changing it requires cantonal or federal supervisory authority approval. That stability suits grant-making institutions and long-term ecosystem stewards. For protocol DAOs that need governance flexibility, it is a real constraint.

How Do the Two Structures Compare Across Key Factors?

The Marshall Islands DAO LLC wins on cost, governance flexibility, on-chain native architecture, and compliance overhead. The Swiss Foundation wins on institutional recognition, banking access, and long-term prestige for grant-making organizations. The table below maps every factor where the choice matters.

What Are the Governance Differences That Actually Matter?

The governance gap between these two structures is the most consequential difference for protocol teams. The Marshall Islands DAO LLC encodes governance in code; the Swiss Foundation embeds governance in a legal hierarchy.

On-Chain vs. Board-Controlled Governance

Under the RMI framework, an operating agreement can point directly to on-chain smart contracts. Token holder votes execute governance decisions. No human intermediary is required to translate community decisions into legal action. The structure explicitly supports manager-less operation, where the protocol's governance logic is the source of legal authority.

The Swiss Foundation routes every governance decision through its Stiftungsrat. Directors owe fiduciary duties to the foundation's stated purpose, which means they can theoretically override a community token vote if they determine it conflicts with those duties. Community governance can be embedded into the foundation's statutes and bylaws, but the board retains ultimate fiduciary and legal authority. For projects where token holder sovereignty is non-negotiable, that gap is fundamental.

Governance Upgradability

Governance models evolve. Token distributions change. The mechanisms that worked at launch often need updating.

The RMI DAO LLC handles this natively: governance rules update through smart contract upgrades, with the operating agreement reflecting those changes through straightforward amendment processes.

The Swiss Foundation's purpose-lock is a structural obstacle. Updating the Zweck requires supervisory authority approval at the cantonal or federal level, a process that can take months and is not guaranteed. For experimental or rapidly iterating governance systems, this rigidity is a meaningful operational risk.

How Do the Tax and Cost Structures Compare?

Both jurisdictions can offer favorable tax treatment, but they arrive at it differently, and the all-in cost picture is very different.

Marshall Islands Tax and Cost

Non-profit RMI DAO LLCs pay zero corporate income tax, zero capital gains tax, and zero withholding tax. There are no mandatory audits, no annual board meetings, no cantonal oversight, and no independent director costs. Annual maintenance through MIDAO covers the registered agent relationship and annual filings. The total annual compliance cost is $2,000-$5,000, all-inclusive.

A key point from the MIDAO incorporation guide: compared to Cayman or Swiss structures, where annual compliance can cost $10,000-$40,000 per year, the RMI structure is dramatically lighter. See MIDAO's pricing page for a full breakdown of registration and annual fees.

Swiss Foundation Tax and Cost

Swiss foundations can achieve tax-exempt status, but it is not automatic for blockchain projects. Blockchain foundations in Switzerland are typically treated as for-profit because their purposes do not qualify as public interest under cantonal law, meaning corporate tax applies. There is no universal crypto-specific tax exemption at the entity level.

Annual costs include mandatory audits (full audit required if assets exceed CHF 20 million), cantonal supervisory fees, Stiftungsrat member costs, and the required Switzerland-domiciled board member. Annual maintenance regularly runs $10,000-$30,000 or more for active protocols.

What Are the Legal Protections for Members and Token Holders?

Both structures protect members from personal liability for the entity's obligations. The differences show up in token treatment and the liability profile of those in governance roles.

RMI DAO LLC Protections

The RMI DAO LLC provides limited liability at the entity level: members are not personally liable for the DAO's debts or legal claims. The 2023 Amendment added an explicit protection against liability for the use of open-source software.

Governance tokens issued by a non-profit RMI DAO LLC, where those tokens carry no economic rights, are explicitly not treated as securities under the RMI statute. That is the strongest statutory securities law carve-out currently available in any DAO-specific jurisdiction.

For most token projects, where no individual holds 25% or more of the token supply, KYC requirements are a non-issue. The typical governance participant provides no personal information at all.

Swiss Foundation Protections

The Swiss Foundation provides entity-level liability protection, and because it has no shareholders or members, individual token holders are not automatically exposed to personal liability through equity-like mechanisms. However, Stiftungsrat members carry personal fiduciary duties under Swiss civil law and can face personal liability for breaches of those duties.

Token treatment under Swiss law depends on FINMA classification. The Swiss Financial Market Supervisory Authority applies a substance-over-form analysis to determine whether tokens are payment, utility, or asset tokens. There is no statutory securities carve-out equivalent to the RMI's 2023 Amendment provision.

Which Structure Fits Which Project?

The Marshall Islands DAO LLC is the better fit for protocol DAOs with active on-chain governance. The Swiss Foundation remains the choice for long-term institutional stewardship, grant-making, and projects where Swiss banking access and European regulatory credibility are strategic requirements.

Choose the Marshall Islands DAO LLC when:

- Governance runs through token voting and smart contracts

- The team wants no mandatory directors, board members, or local presence

- Cost efficiency is a priority, and $10,000-$30,000+ in annual overhead is not justified

- The non-profit governance token securities carve-out is strategically valuable

- Formation speed matters: the process completes in under 30 days

Choose the Swiss Foundation when:

- The project is a long-term grant-making institution or ecosystem steward

- Swiss banking relationships and European institutional credibility are non-negotiable

- The Stiftungsrat governance structure serves the project's accountability needs

- The founding team can absorb $15,000-$50,000+ in setup costs and ongoing annual overhead

- MiCA compliance planning for EU-facing operations benefits from Swiss legal certainty

Marshall Islands DAO LLC vs. Swiss Foundation: Final Verdict

The Swiss Foundation built Crypto Valley. The Marshall Islands DAO LLC was built for what comes next.

The Swiss Foundation is not the wrong choice for all projects. For the Ethereums and Solanas of the world, building long-term infrastructure with institutional backers, the Swiss structure's credibility and banking access justified every dollar of overhead. Those projects also incorporated before algorithmic, manager-less governance was a realistic legal option.

For protocol DAOs being built today, the calculus is different. The RMI DAO LLC delivers legal personhood, liability protection, a statutory securities carve-out for governance tokens, manager-less operation, and a total compliance cost that is a fraction of the Swiss alternative. It is not a compromise; it is a purpose-built solution for how decentralized governance actually works.

The Swiss Foundation's purpose-lock, mandatory board, local presence requirement, and $10,000-$30,000+ annual overhead make it the right answer for a specific type of project. For most protocol DAOs prioritizing on-chain governance, token flexibility, and operational simplicity, the Marshall Islands DAO LLC is the more rational structure.

Ready to incorporate your DAO in the Marshall Islands? Start the process with MIDAO, the only government-authorized registration program for RMI DAO LLCs, and get your entity registered in under 30 days.

Frequently Asked Questions

How does each structure handle governance upgrades when the underlying token model changes significantly?

The Marshall Islands DAO LLC handles governance upgrades natively: the operating agreement can reference updated smart contracts, and token model changes can be reflected through amendment processes without external approval. The Swiss Foundation's purpose lock (Zweck) requires cantonal or federal supervisory authority approval to change, making significant governance pivots slow and structurally difficult. For projects with evolving or experimental governance systems, the RMI structure offers dramatically more flexibility.

Can a project migrate from a Swiss Foundation to a DAO LLC without breaking token holder rights or legal continuity?

Migration is possible but requires careful structuring: the Swiss Foundation holds and then transfers assets, intellectual property, and contractual relationships to the new RMI DAO LLC entity. Token holder rights are determined by the project's token contracts rather than the legal wrapper, so a well-designed migration can preserve on-chain governance continuity. The legal restructuring involves cantonal supervisory authority coordination to dissolve or repurpose the foundation, which adds time and cost. MIDAO can structure the incoming RMI entity; Swiss counsel must handle the outgoing foundation side.

How do each of these structures interact with US-based token holders from a liability perspective?

Neither the Marshall Islands DAO LLC nor the Swiss Foundation creates automatic personal liability for US-based token holders simply through token ownership. The RMI non-profit structure includes a statutory carve-out providing that governance tokens with no economic rights are not treated as securities under RMI law, which is the strongest available statutory protection. US-based token holders in either structure should still obtain independent US legal advice on their own tax and securities law obligations, which are determined by US federal law regardless of where the entity is domiciled.