Marshall Islands DAO LLC vs. Cayman Foundation: Full Comparison

A comparison of the Marshall Islands DAO LLC and Cayman Foundation, focusing on governance, tax benefits, costs, and legal structures to help DAOs choose the right framework.

According to the DAO Development Market Outlook Report, Intel Market Research, Q3 2024, the global DAO development market was valued at $170 million in 2024 and is projected to reach $333 million by 2031, at a compound annual growth rate of 9.3%.

That growth means more DAOs are making high-stakes decisions about legal structure, often without a clear framework for comparison. Two options dominate the conversation for globally distributed Web3 teams: the Marshall Islands DAO LLC and the Cayman Islands Foundation Company. Both are tax-neutral. Both provide legal personhood. Both have been used by serious crypto projects.

But they are not interchangeable. The right choice depends on your governance model, your tolerance for ongoing overhead, and how much structural weight you want sitting between your community and your legal wrapper. This article breaks down the key differences so your team can make an informed decision.

What Are the Two Structures?

The Marshall Islands DAO LLC and the Cayman Foundation are the two most widely used offshore crypto structures for DAOs. One was purpose-built for decentralized organizations; the other was adapted from foundation company law to serve the Web3 ecosystem.

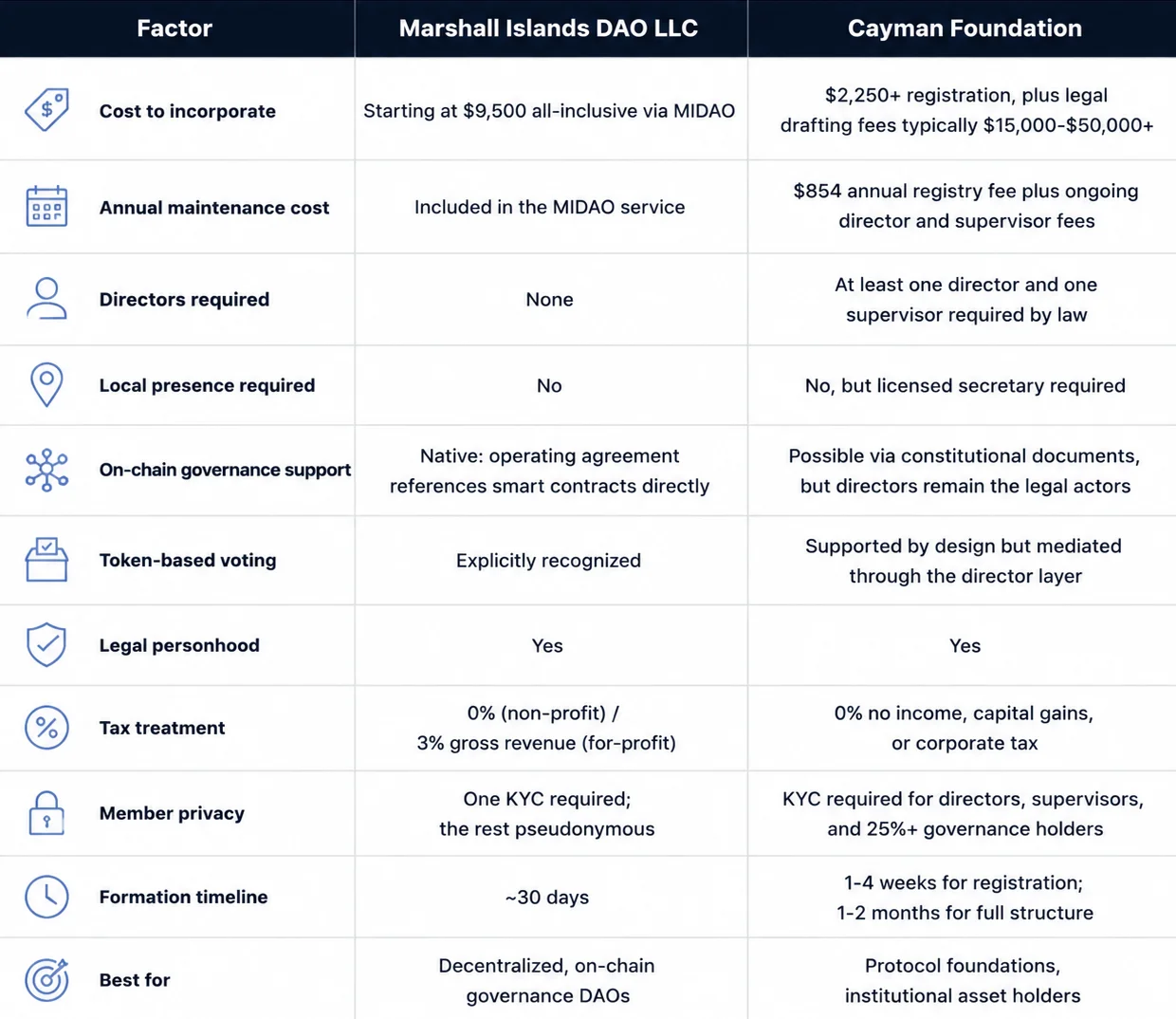

The Marshall Islands DAO LLC

The Republic of the Marshall Islands enacted the DAO Act of 2022, becoming one of the first sovereign nations to grant DAOs explicit legal personhood as limited liability companies. The framework has since been updated by a 2023 Amendment, which added Series DAO LLC capability, and the 2024 Regulations, which clarified KYC thresholds and on-chain compliance requirements.

The RMI structure is built around the principle that a DAO's on-chain governance is the governance. Operating agreements can reference smart contracts directly, governance tokens are recognized as a valid decision-making mechanism, and no directors, officers, or local representatives are required. The DAO's community governs. That is the design, not a workaround.

MIDAO operates as the exclusive public-private partnership with the RMI government for DAO LLC registration, making it the authoritative channel for this framework.

The Cayman Foundation Company

The Cayman Islands introduced the Foundation Companies Law in 2017, and the structure has since become one of the most widely used DAO legal wrappers globally. A Cayman Foundation is a company without shareholders: it is purpose-driven rather than profit-distributing, which aligns well with the ethos of many protocol-focused DAOs.

The foundation must be managed by at least one director and supervised by at least one supervisor. These roles carry fiduciary duties to the foundation's stated purpose. Governance can be designed to reflect token-holder voting, and constitutional documents can link on-chain decisions to off-chain legal authority. However, the directors, not the smart contracts, remain the legally operative layer.

Both structures offer tax neutrality. Both are recognized internationally. But their internal architecture is meaningfully different in ways that affect cost, governance design, and operational simplicity.

How Do the Marshall Islands DAO LLC and Cayman Foundation Differ on Key Factors?

What Are the Governance Differences?

The Marshall Islands DAO LLC supports fully decentralized governance natively. The Cayman Foundation requires a human director layer between community decisions and legal execution.

Marshall Islands DAO LLC Governance

Under the RMI framework, an operating agreement can point directly to the DAO's on-chain governance contracts. Token holder votes, smart contract execution, and community proposals carry formal legal weight without requiring a parallel off-chain approval process. Projects like Pyth DAO use exactly this structure: the Marshall Islands DAO LLC operating agreement references the protocol's governance smart contracts, giving those contracts real legal authority.

There is no required management function. The DAO's members, acting through their governance tokens, are the operative governing body. This is not just philosophically aligned with decentralization; it is structurally encoded.

Cayman Foundation Governance

A Cayman Foundation can be designed to reflect token-holder governance through its constitutional documents and bylaws. Directors are legally required to take instructions from the DAO and act on approved proposals. In practice, this means the DAO votes, and then the directors execute.

That intermediary layer is a meaningful difference. The directors owe fiduciary duties to the foundation's stated purpose, which provides governance guardrails. But it also means the community's on-chain decisions are filtered through off-chain human actors before they carry legal force. For DAOs where full on-chain autonomy is a priority, this friction is a genuine trade-off.

How Do the Legal Protections Compare?

Both structures provide limited liability protection, legal personhood, and asset protection. The meaningful differences are in who carries KYC obligations and what happens when governance decisions face legal scrutiny.

Marshall Islands DAO LLC Protections

The RMI DAO LLC grants the entity full legal personhood: it can own assets, sign contracts, appear in court, and absorb liability without those consequences flowing through to individual members. Only one beneficial owner is required to complete KYC, and that person can be located anywhere in the world.

The 2023 Amendment added explicit protection against liability for use of open-source software, and Series DAO LLC's capability allows sub-DAOs to hold segregated assets and liabilities.

Members beyond the single KYC-verified owner can remain pseudonymous under the RMI framework. For decentralized communities with hundreds or thousands of governance participants, this is a significant practical advantage.

Cayman Foundation Protections

The Cayman Foundation provides comparable entity-level liability protection. Assets held by the foundation are ring-fenced from the personal liabilities of its directors and supervisors. Every director, supervisor, and any governance token holder with 25% or more of voting rights must undergo KYC under Cayman rules.

Cayman's legal system, based on English common law, is deeply familiar to institutional investors, law firms, and financial counterparties. For projects seeking institutional capital or exchange listings that require Cayman-based entities, this familiarity is a meaningful operational asset. The trade-off is a larger compliance surface and higher ongoing professional costs.

What Are the Tax and Cost Implications?

Both jurisdictions are tax-neutral for non-profit structures. The gap between them is in ongoing compliance cost, not the tax rate itself.

Marshall Islands Tax Structure

Non-profit RMI DAO LLCs pay zero corporate income tax, capital gains tax, and withholding tax, with no mandatory annual tax filings. For-profit DAO LLCs pay a 3% gross revenue levy, excluding dividends and capital gains. There are no economic substance requirements: the DAO does not need to maintain physical offices or staff in the RMI to benefit from the framework.

MIDAO's all-inclusive service starts at $9,500, covering registration, operating agreement workshops, and ongoing compliance support with no hidden fees.

Cayman Foundation Tax Structure

The Cayman Islands imposes no income, corporate, capital gains, or inheritance tax. Foundation companies limited by guarantee are excluded from Cayman's economic substance regime, so there is no requirement to relocate operations or staff to the islands.

The cost picture is different from the RMI. Registry fees alone run $609 for incorporation and $854 annually. Legal drafting of constitutional documents, bylaws, and governance frameworks through Cayman-licensed counsel typically adds $15,000 to $50,000 or more, depending on complexity. Ongoing director and supervisor fees from licensed service providers add further annual overhead. For early-stage projects or lean teams, this cost structure is a real barrier.

Which Structure Fits Which DAO?

The Marshall Islands DAO LLC is the stronger fit for community-governed, on-chain-first DAOs seeking cost efficiency and governance simplicity. The Cayman Foundation suits complex, institutional, or multi-stakeholder structures where English common law familiarity and a formal director layer are assets rather than obstacles.

Choose the Marshall Islands DAO LLC when:

- The DAO's governance runs primarily on-chain through token voting and smart contracts

- The team wants to minimize mandatory professional appointments and associated costs

- Member privacy is a priority, and pseudonymous participation is the norm

- The project is early-stage or cost-sensitive and needs a clean, all-in structure

Choose a Cayman Foundation when:

- The project requires institutional recognition familiar to large investors and exchanges

- The DAO involves complex asset structures or multi-entity arrangements

- A formalized director layer adds governance accountability that stakeholders value

- The project is prepared to absorb higher legal and ongoing compliance costs

For most decentralized protocols, the Marshall Islands DAO LLC offers a more direct path to legal protection without the structural overhead that the Cayman Foundation requires by law.

Cayman Foundation vs. DAO LLC: Final Verdict

The most important insight from this comparison is structural: the Marshall Islands DAO LLC was designed for DAOs from the ground up, while the Cayman Foundation was adapted from existing company law to serve them. That difference shows up concretely in cost, governance design, and director requirements.

The Cayman Foundation is a proven and respected structure, particularly for projects with institutional stakeholders, complex treasury arrangements, or exchange-listing requirements that favor Cayman entities. Its flexibility and English common law grounding make it the choice for projects where the director layer is an asset, not a cost.

The Marshall Islands DAO LLC wins on the four factors that matter most to community-governed projects: lower all-in cost, no required directors or supervisors, native on-chain governance recognition, and a simpler ongoing compliance profile. For globally distributed DAOs running on-chain governance, it is a more purpose-aligned structure.

Explore whether the Marshall Islands DAO LLC is the right fit for your project. Review MIDAO's pricing and structure options, or book a free consultation with the MIDAO team to get expert guidance tailored to your DAO's governance model.

Frequently Asked Questions

1. What is the main governance difference between a Marshall Islands DAO LLC and a Cayman Foundation?

The Marshall Islands DAO LLC allows on-chain governance to operate as the legal governance layer directly, with operating agreements pointing to smart contracts and token votes carrying formal legal authority. A Cayman Foundation routes community decisions through a board of directors who are legally required to act on approved proposals, adding a human intermediary layer between on-chain governance and legal execution.

2. Can a Marshall Islands DAO LLC be used for asset protection purposes?

Yes. The RMI DAO LLC provides entity-level asset protection: assets held by the DAO LLC are separate from the personal liabilities of its members. The 2023 Amendment also introduced Series DAO LLC capability, allowing a parent DAO to establish sub-DAOs with their own segregated asset pools and liabilities, which is particularly useful for multi-protocol or multi-product organizations.

3. How does the tax treatment of a Marshall Islands DAO LLC compare to a Cayman Foundation?

Both jurisdictions are tax-neutral at the entity level: neither imposes corporate income tax, capital gains tax, or withholding tax on non-profit structures. The practical difference is in compliance cost, not tax rates. Non-profit RMI DAO LLCs have no mandatory annual tax filings. Cayman Foundations pay annual registry fees, require licensed directors and supervisors, and typically incur significantly higher ongoing professional costs, making the all-in cost of the Cayman structure materially higher for most DAOs.